Romana King

Updated Dec 23, 2025

If you’re in your 40s or 50s you may appreciate the debt versus savings dilemma. As you juggle the responsiblity of paying down a mortgage, while saving to accumulate a retirement nest egg, you may also feel the pressure of debt. Thing is: you're not alone.

The question remains: is it better to pay off debt, first, or save up for retirement?

Now, the urge to become debt-free is strong — really strong. It feels responsible, safe, and immediately satisfying to pay off debt, particularly large debt such as a mortgage on a house. But what if the rush to pay off low-interest debt is quietly undermining your long-term retirement security? While there is no one right answer, tax expert Jamie Golombek argues that paying down debt actually puts your retirement at risk. In his report, Mortgages or Margaritas: Is paying down debt putting your retirement at risk? (1) he suggests that the urge to pay down debt rather than contribute to a tax-efficient savings vehicle, such as a registered retirement savings plan (RRSP), is more about appeasing emotions than making smart money decisions (2).

The emotional pull of debt freedom

In this report, Golombek surveyed Canadians to help understand what drove them to prioritize debt repayment over saving for retirement. The survey data revealed just strong the emotional pull is for Canadians to become debt-free. Among Canadians asked what they'd do if they had extra funds to spare, 72% of those aged 35 to 54 picked “pay down debt” over “add to an RRSP” (3). A further 56% confessed that the main reason was a simple desire for “the financial freedom of being debt-free.”

As Golombek points out: There’s nothing wrong with that desire — it’s human, understandable — but it highlights a gap between what feels safe and what might mathematically build retirement security (4).

Sponsored

Smart investing starts here

Build your own investment portfolio with CIBC Investor’s Edge online and mobile trading platform. Enjoy low commissions on trades and special pricing for active traders, students and young investors.

Get started todayThe mathematical case: Investing often wins

To illustrate, let's assume you have $2,500 of extra pre‐tax earnings each year. You could either apply that toward extra mortgage payments, assuming a 4% mortgage rate, or invest in your RRSP or Tax Free Savings Account (TFSA). For simplicity, we'll assume the RRSP investment earns a 6% annualized investment return over 30 years.

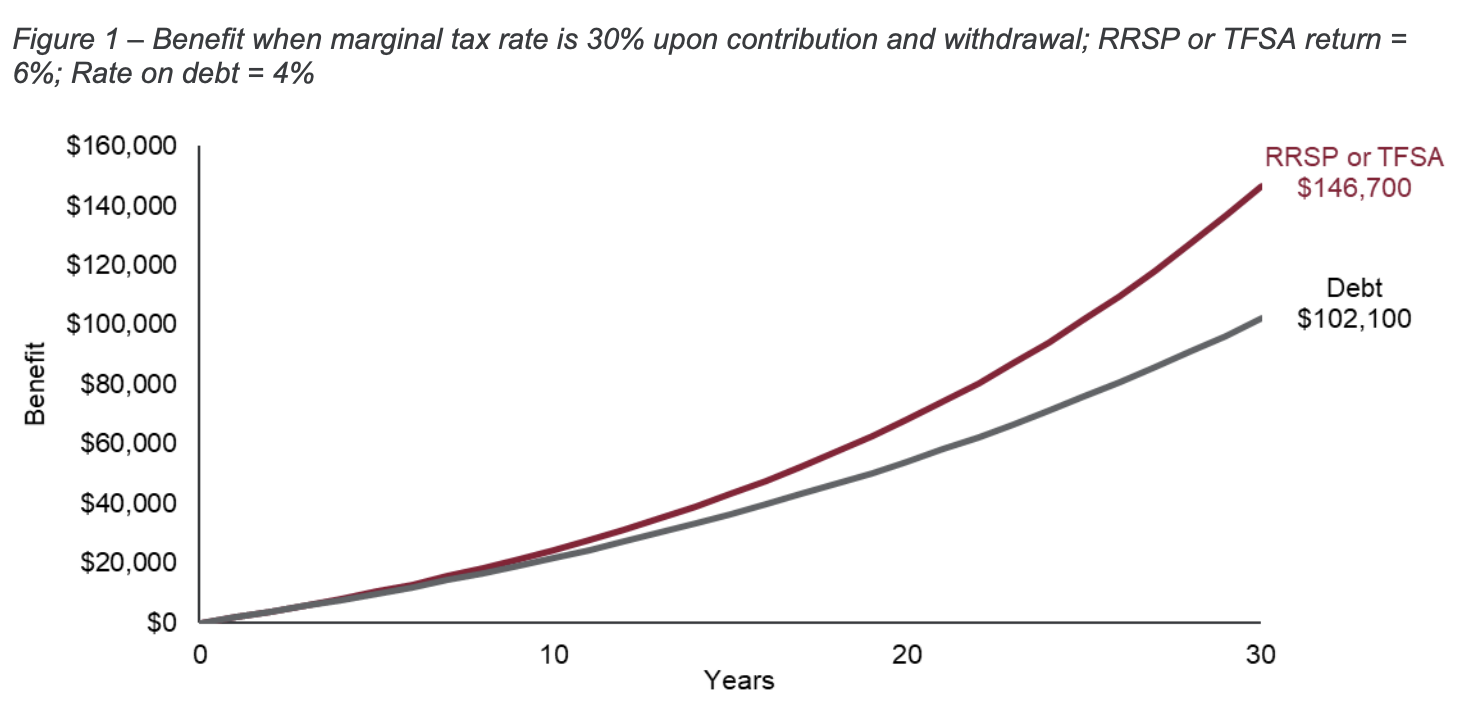

If your marginal tax rate stays the same in retirement

If your marginal tax rate, today, was 30% and the early withdrawal rate is the same, then investing would put you almost $45,000 ahead as the decision to pay down debt, according to Golombek's calculations (5).

If your marginal tax rate drops in retirement

If you expect your tax rate to drop in retirement — going from 30% to 20% — the RRSP strategy improves your investment portfolio, boosting it from $ 146,700 to about $167,600 (6). As Golombek explains: if your expected investment return (after tax) exceeds the interest rate on your debt, investing may give you more in the long run.

When paying debt first still makes sense

This isn’t to say you should always invest and never attack debt. If you’re carrying high-interest debt, such as a credit card balance, or lines of credit at 20% or more interest, then paying this debt off first is almost always the best option.

Golombek identifies another reason why tackling debt first makes sense: if you’re very leveraged and wouldn’t weather a rate increase or economic shock, then reducing risk via debt repayment is prudent.

Sponsored

Take control of your money with Monarch

Simplify your finances with Monarch, the all-in-one app designed to help you budget, track spending, and hit your goals faster. For a limited time, get 50% off your first year with code WISE50.

Start your free trial todayThe competing goals of a homeowner/saver

For a mid-career homeowner who has a mortgage and still unsure whether to tackle debt or invest in your RRSP savings, the critical questions to answer include:

1. What is my mortgage interest rate? Is your mortgage rate higher than 5%?

YES→ Begin leaning toward paying down the mortgage, unless you expect exceptionally high RRSP returns and have a long time horizon.

NO → Rates below 5% often favour RRSP investing, especially with tax benefits and compounding.

2. What return can I reasonably expect from investing in my RRSP (net of tax)? Estimate expected long-term investment return (e.g., 4% to 6% real return for a balanced/growth portfolio), then compare that to your mortgage rate. Is your expected RRSP return (after tax) higher than your mortgage rate by at least 1% to 2%?

YES → Advantage RRSP → continue to next question.

NO → Advantage debt repayment → continue anyway for confirmation.

3. What is my time horizon until retirement? More than 15 years to retirement?

YES → RRSP investing becomes more attractive because compounding has time to work.

NO → Mortgage repayment becomes more attractive, especially if nearing retirement and wanting a lower cost base.

4. What is my tax rate now, and what do I expect it to be in retirement? RRSPs are most powerful when your tax bracket today is higher than your expected tax bracket later (say, in retirement). Is your tax rate now significantly higher than what you expect in retirement (at least one bracket difference)?

YES → RRSP advantage. RRSP contributions defer tax at a high rate and withdrawals will be taxed at a lower rate.

NO → Debt repayment advantage. The RRSP tax deferral is less impactful.

5. What is my comfort level with investment risk and debt levels? Do you feel stressed carrying debt or prefer guaranteed returns?

YES → Pay down mortgage.

NO → RRSP investing is reasonable.

6. Do you have a long investment horizon and can tolerate market volatility?

YES → RRSP investing becomes more favourable.

NO → Mortgage repayment provides a risk-free, “guaranteed” return equal to your interest rate.

Focus on RRSP investing

If you answered "Yes" to most of the following:

- Mortgage rate under 5%

- Expected RRSP returns exceed mortgage rate

- More than 15 years to retirement

- Higher tax bracket now than in retirement

- Comfortable with investment risk and debt

... then you should focus on investing in your RRSP (or TFSA). Why? Because investing in your retirement savings plan helps you maximize compounding, tax savings, and future flexibility.

Focus on mortgage repayment

If you answered "Yes" to most of the following:

- Mortgage rate above 5%

- Expected RRSP return similar to or below mortgage rate

- Less than 15 years to retirement

- Similar tax bracket now and later

- You dislike debt or prefer guaranteed returns

... then you should focus on paying down the mortgage. Why? Because paying down this large debt is a risk-free return equal to your interest rate — and reduces financial pressure in retirement.

“If you have a high mortgage interest rate, you might save more by paying down your mortgage rather than investing in your RRSP,” explains Michael Callahan, an Edward Jones analyst, and financial advisor (7).

Consider tax implications

RRSP contributions generate an immediate tax deduction and allow you to defer tax payment until you withdraw from this fund. This is what makes RRSP contributions so powerful — but only if you anticipate your tax rate to be lower in retirement than during your employment years. Plus, mortgage interest on a principal residence is not tax-deductible in Canada, so the benefit of debt repayment is purely the interest cost avoided.

Factor in time horizon and risk tolerance

If retirement is 15 or more years away and you’re comfortable with market risk, investing may be effective. However, if the time horizon is shorter, or you prefer certainty and lower risk, reducing debt may feel more aligned.

Consider liquidity and flexibility

Funds invested in an RRSP aren’t as easily accessible as cash reserves. If you foresee needing cash for emergencies, make sure you have an emergency fund before allocating everything to RRSPs or debt.

Pay off mortgage and invest in RRSP

Quite often you don’t need an either-or decision. By contributing some money to your RRSP and making some extra payments towards paying down your debt, you can achieve a balanced approach to savings and debt repayment. This balanced path preserves growth and reduces leverage.

Split strategy (recommended for most people)

Choose this balanced approach if your answers to the questions are a mix of yes and no. For example:

- Your mortgage rate is around 4% to 5%

- Medium risk tolerance

- 10 to 20 years to retirement

- Hard to predict future tax bracket

Strategy: Put a portion of available money into RRSPs (to capture tax benefits) and a portion into extra mortgage payments.

Why it matters for retirement

For a homeowner in their 40s or 50s, time is both an asset and a constraint. You’re likely earning peak income, tax brackets may be high, and you still have 15 to 20 years until typical retirement. Choosing to delay RRSP contributions or redirect surplus funds purely to mortgage pay-down could mean missing significant growth and tax-sheltered compounding. "Neglecting your long-term savings in favour of debt repayment may result in sacrificing the quality of your retirement,” explains Golombek (8).

Bottom line

For many Canadian homeowners, the urge to eliminate debt is strong — and for good reason. But it’s vital to check the math and not let emotion lead the decision. Ask yourself: can my investments realistically deliver a higher effective return (after tax) than the interest cost of my debt? If yes — and if you’re comfortable with some risk, have time until retirement, and aren’t weighted by high-interest liabilities then shifting some of your extra dollars toward your RRSP may make more sense than throwing every cent at the mortgage. If the opposite holds, prioritize repayment. And if you don’t want to choose, do both.

In short: paying off debt feels great. Investing may feel riskier. But in the long game of retirement, it’s the disciplined, strategic decision-making that builds real wealth — and the emotional satisfaction of being debt-free doesn’t substitute for decades of missed opportunity.

Article sources

We rely only on vetted sources and credible third-party reporting. For details, see our editorial ethics and guidelines.

CIBC (1, 5, 6); CIBC (2, 3, 4); Edward Jones (7); Jamie Golombek (8)

How Dave Ramsey’s plan helps people ditch debt for good

Tired of living paycheck to paycheck? Dave Ramsey’s popular 7-step method shows you exactly how to wipe out debt and finally build real savings. No gimmicks — just a clear plan that works.

Romana King

Senior Editor

Romana King is the Senior Editor at Money.ca. She writes for various publications, and her book -- House Poor No More: 9 Steps That Grow the Value of Your Home and Net Worth -- continues to be an Amazon bestseller. Since its publication in November 2021, this book has won five awards, including the New York CPA Society's Excellence in Financial Journalism (EFJ) Book Award in 2022.

Explore the latest articles

Breaking down Canada's alphabet soup of retirement

Knowing which programs you can count on in old age will help you plan for retirement.

Sigrid Forberg

Associate Editor

Disclaimer

The content provided on Money.ca is information to help users become financially literate. It is neither tax nor legal advice, is not intended to be relied upon as a forecast, research or investment advice, and is not a recommendation, offer or solicitation to buy or sell any securities or to adopt any investment strategy. Tax, investment and all other decisions should be made, as appropriate, only with guidance from a qualified professional. We make no representation or warranty of any kind, either express or implied, with respect to the data provided, the timeliness thereof, the results to be obtained by the use thereof or any other matter. Advertisers are not responsible for the content of this site, including any editorials or reviews that may appear on this site. For complete and current information on any advertiser product, please visit their website.

†Terms and Conditions apply.